Emerging Europe’s Convergence: 20 Years of Growth and What Comes Next

Two Decades of EU Integration: A Success Story

In May this year we celebrated the 20th anniversary of European Union enlargement that saw 10 Emerging Europe countries (Czechia, Estonia, Cyprus, Latvia, Lithuania, Hungary, Malta, Poland, Slovenia and Slovakia) and over 74 million citizens integrating into the EU. Less than 3 years later Bulgaria and Romania joined, while Croatia reached the membership status in 2013.

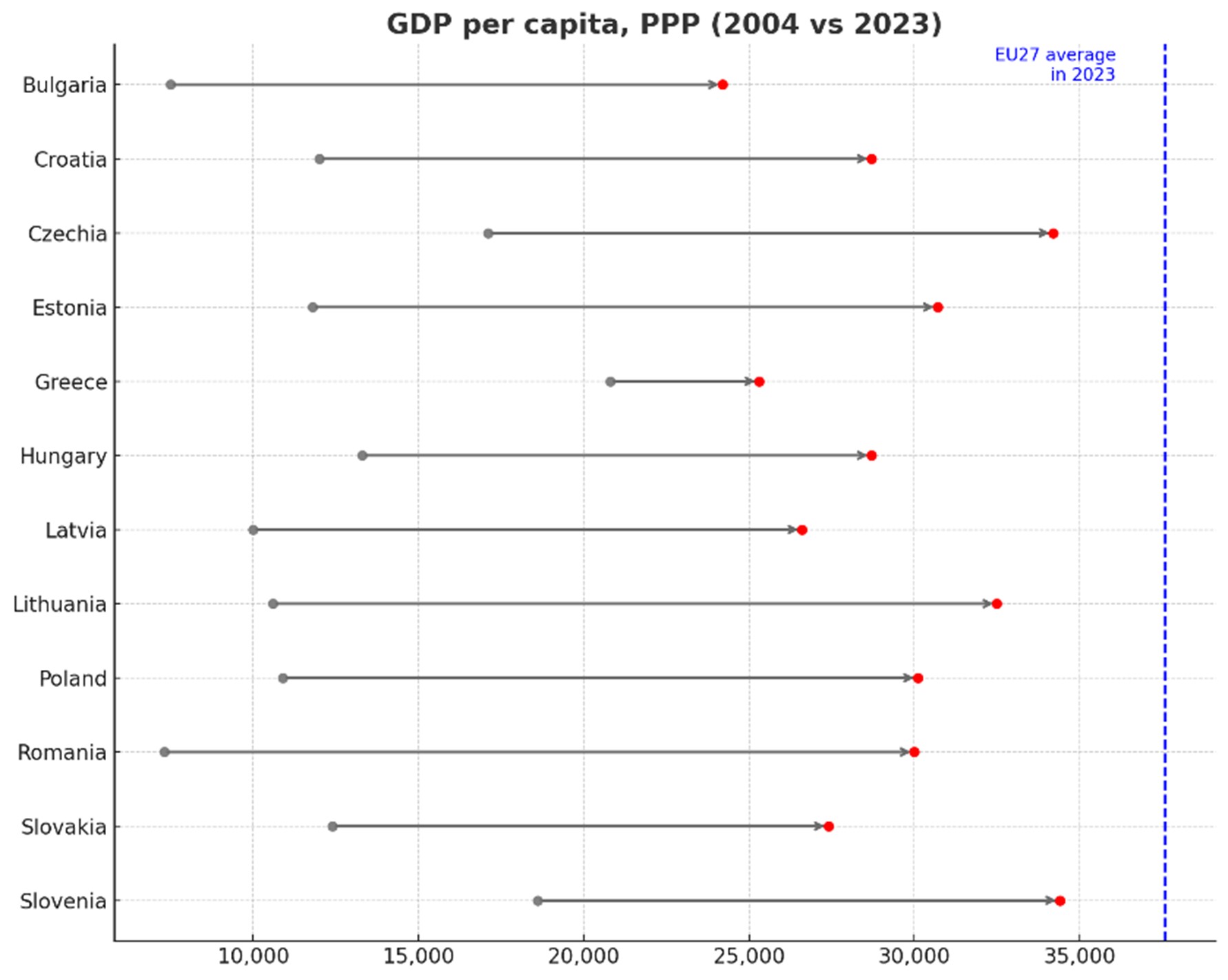

Looking back, the integration of Emerging European countries has proven to be an economic success, supported by the EU’s Cohesion Policy. Over the past two decades most of the new member countries have managed to more than double their GDP per capita (PPP) and reached nearly 80% level of the EU average in 2023 from around 50% in 2004.

Based on the pre-Covid (2019) GDP data the share of Emerging Europe in EU economy was only 12%, however the region accounts for 25% of EU’s population and 30% of the area.

Source: Eurostat

Economic Progress and Labour Market Transformation

At the same time, the unemployment rate in the region has dropped from around 15% level to below 5%, while income gap has narrowed. Based on income classifications by the World Bank, in 2023, most EU member Emerging Europe countries had achieved the status of high-income countries ($14,005 GNI per capita). This success can be attributed to enhanced institutional quality, supported by the EU accession, combined with a plentiful supply of low-cost well-educated labour. These elements have facilitated an influx of foreign capital, more efficient resource allocation, and impressive productivity growth.

Source: Eurostat and DG REGIO calculations

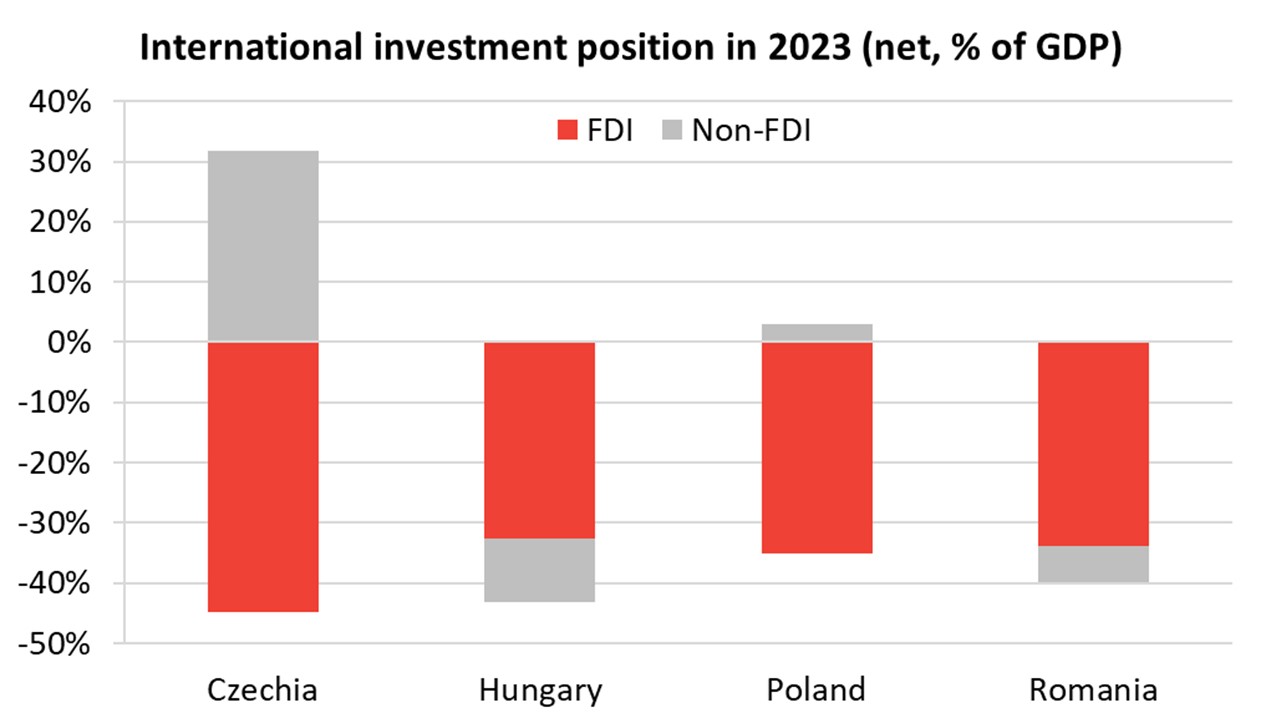

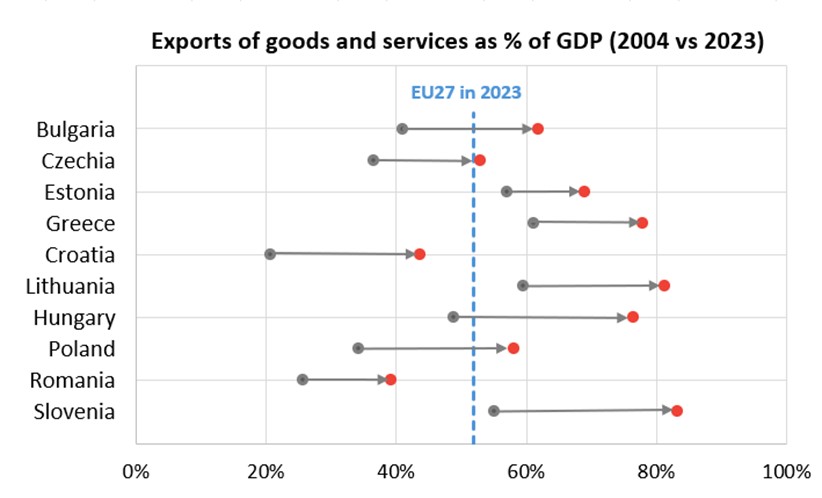

The cornerstone of Emerging Europe’s success has been its export-led growth model that capitalized on the existing industrial base. This contrasts to the credit-led and domestic-oriented growth model seen previously in Southern Europe. Both have been and are dependent on capital inflows due to limited capital and modern technology. However, the nature of these inflows has differed. Southern Europe primarily relied on credit, whereas Emerging Europe attracted foreign direct investment (FDI). The graph below depicts the net international investment position for select regional countries. The level of non-FDI net foreign debt is almost negligible. In fact, Czechia and Poland are even net creditors.

Source: Eurostat

Source: Eurostat

Low Indebtedness and Capital Market Opportunity

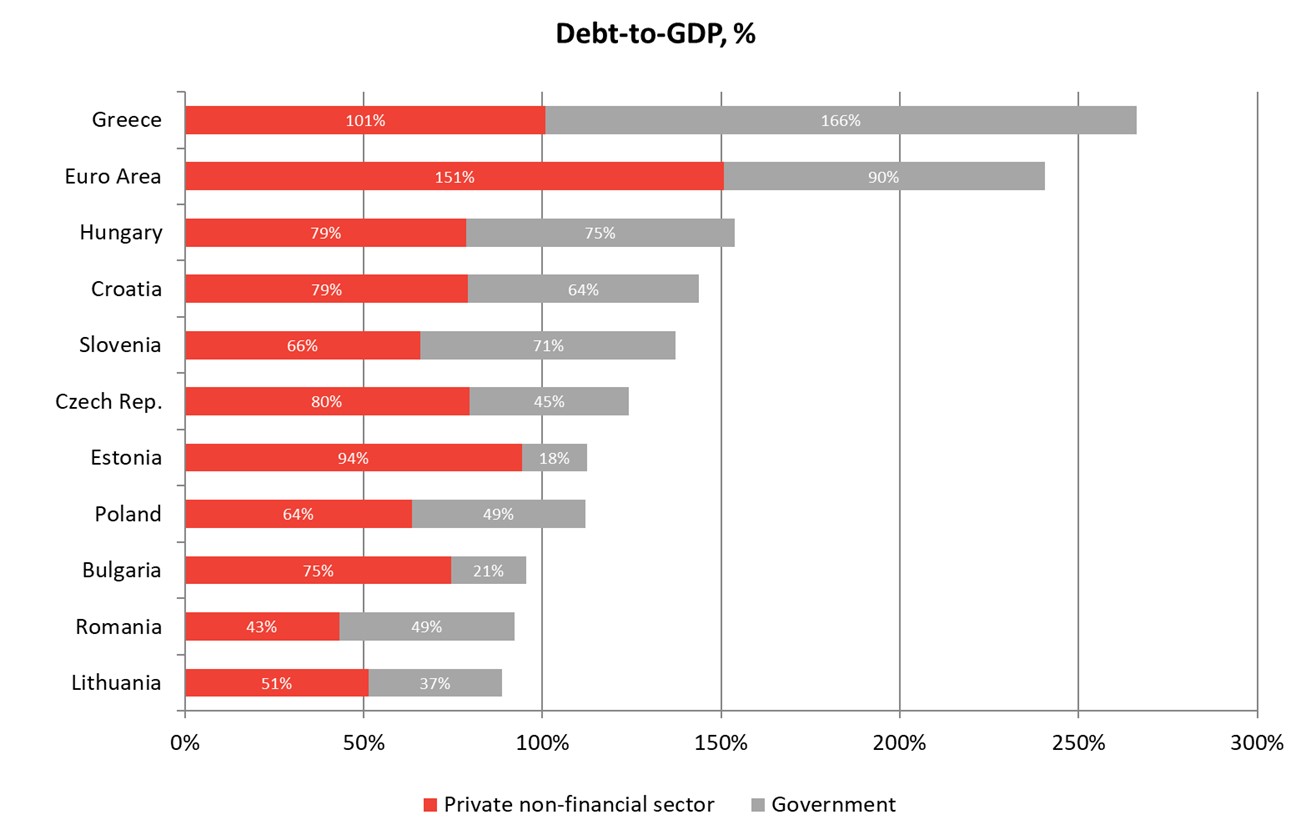

In addition, the indebtedness of Emerging Europe countries, illustrated in the graph below, is low, both on private and public sector level.

Source: Eurostat, LSEG

The experience of the past decade, including insights from the European debt crisis, underscores the risks associated with excessive reliance on foreign debt. Such capital inflows are highly reversible, and the cost of servicing external debt can often be influenced by external factors rather than domestic economic fundamentals. In this context, the relatively low level of indebtedness in Emerging Europe countries provides considerable room for capital deepening and growth through credit expansion. We would even argue that regional countries are underleveraged and underutilise their potential. Developing capital markets further can help high-growth companies access funding for scaling operations, particularly in technology and green sectors. Over the past few years we have already seen a notable step forward in local bond market development, which until recently was almost non-existent.

Industrial Convergence: The German Connection

Emerging Europe economies have benefited greatly from foreign direct investment (FDI), which has provided not only capital but also modern management practices and technology transfers. Germany has played a significant role in this regard as German companies have established a number of manufacturing units in the region, especially in automotive, electronics and machinery sectors. This industrial convergence and integration into supply chains have boosted regional productivity gains. Countries like the Czech Republic, Romania and Slovakia have become crucial parts of the European automotive and machinery supply chains, helping to drive industrial efficiency and specialization. This has underpinned the robust export growth in the region over the past two decades.

Supply Chain Shifts and Labour Market Efficiency

Post pandemic Emerging Europe overall has benefitted from businesses’ reorganization of supply chains and reshoring of production activities as companies seek cost-efficient, closer-to-home manufacturing and assembly locations within the EU. According to the EY’s recent study, the number of manufacturing investment projects (greenfield and expansionary) decreased slightly across Europe last year in comparison to 2022. However, increases were seen in Czechia, Hungary, Poland, Serbia and Turkey.

Source: Eurostat

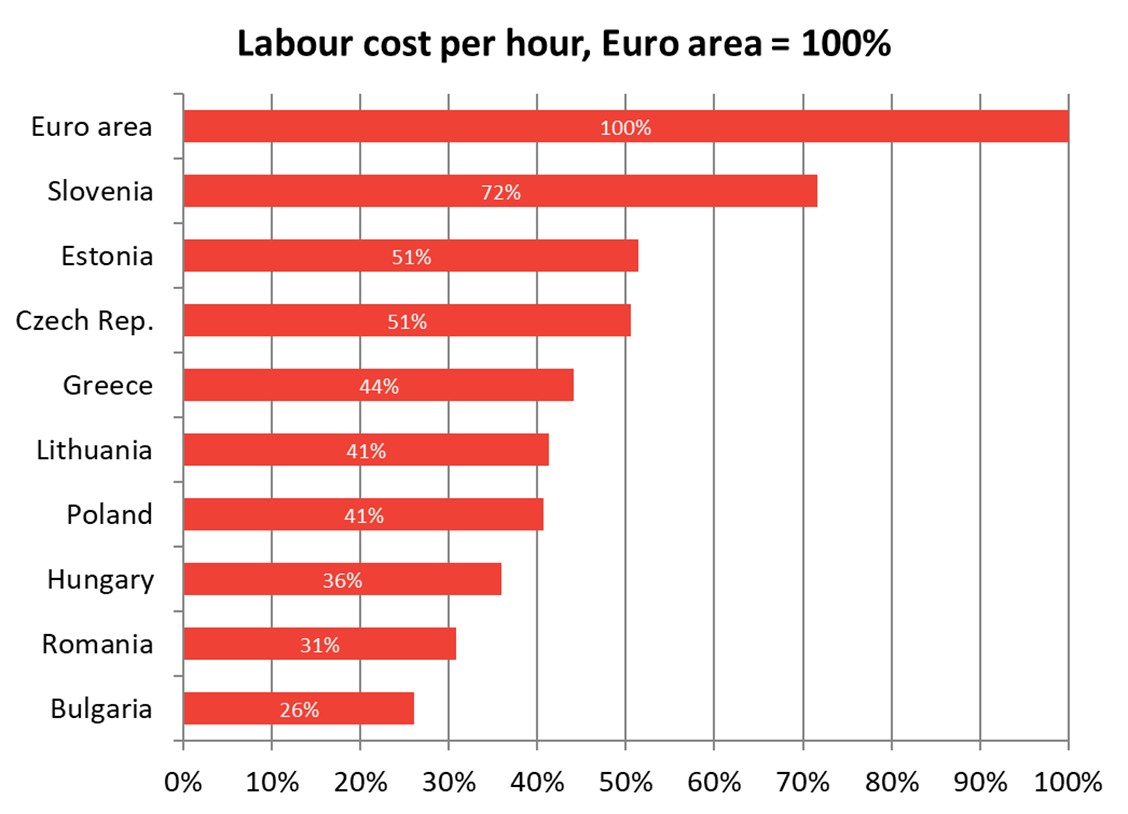

Another important driver of convergence and region’s competitiveness has been the increased labour market efficiency and improved educational level over time. While labour costs have risen, they remain low compared to Western Europe. At the same time, the skill level and education of the workforce in the region have been steadily improving, leading to gains in productivity.

Source: Eurostat

Productivity Is Now the Key Growth Driver

Given the challenging demographic situation in Emerging Europe, which is similar to Western Europe, productivity gains have been instrumental in Emerging Europe’s convergence and retaining its competitiveness.

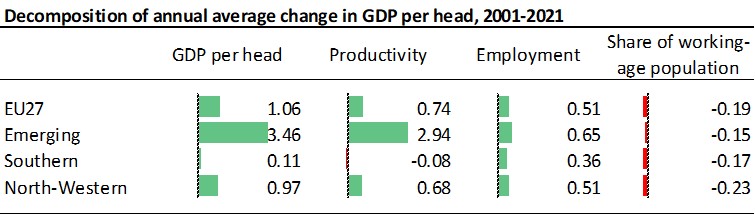

Growth in GDP per capita can be broken down into three main components – changes in productivity (GDP per person employed), changes in the employment rate (employment relative to population of working age) and changes in the share of working age population in the total.

The same can be expressed in terms of changes: the change in GDP per head is the sum of the changes in productivity, in the employment rate and in the share of working age population. European Commission published its 9th Cohesion Report back in March, which highlighted the historical importance of productivity gains as a growth driver in Emerging Europe.

Source: Eurostat, ARDECO, Cambridge Econometrics, AMECO, DG REGIO calculations

We believe that the factors outlined above will continue to play a significant role in the future, although it could be argued that much of the readily attainable benefits have already been realized. Academic research has shown that within the export-led growth model, export expansion is supported by undervalued exchange rates and competitive wages, the transfer of foreign technologies, and partnerships between countries and multinational corporations. The success thus depends on access to foreign technologies and markets, robust foreign demand and the availability of a well-educated labour force that can be hired at internationally competitive wages.

As we noted above the income gap has narrowed notably, however, the wage levels in the region are still significantly below the Eurozone. With labour markets becoming more efficient, employment rates in several countries close to the high level of Germany (81%), and unemployment levels across the board at historical lows, the availability of workers has become an increasingly important factor for future economic expansion. Especially, given the demographic challenges of aging and decreasing population. By 2030, the population aged 20-64 is projected to shrink by 2% in Czechia and Hungary, and by 5% in Poland and Romania.

Besides migration policies that allow non-EU citizens to enter the labour market, there are tentative signs that the reversal of brain drain, witnessed in the past, is starting to gain traction. In recent years, a growing number of workers have returned to Emerging Europe, attracted by the increased opportunities available and the improved living standards. This should alleviate the pressure on the tight labour market.

Innovation: The Next Frontier

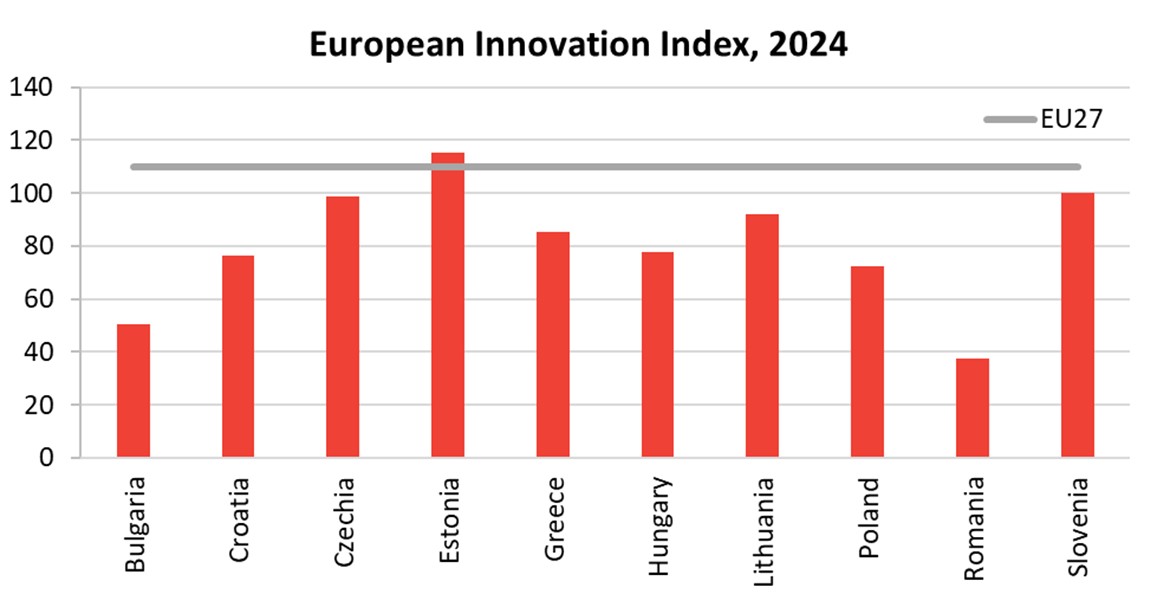

One area where we see significant room for improvement is innovation and R&D spending. According to the European Commission’s European Innovation Scoreboard (EIS), the overall performance of Emerging Europe countries is well below the EU average.

Source: EIS interactive tool 2024

Source: EIS interactive tool 2024

In the past Emerging Europe countries have been more successful in adopting existing technologies than developing their innovation potential. Now, if growth through infusion is starting to reach its limits, a reorientation towards an innovation-supportive approach is required. Given that Emerging Europe has a well-educated labour force that is positioned to support high value-added sectors, regional countries can enhance productivity by fostering innovation, automation, and adopting AI-driven solutions.

Green Transition: From Coal to Clean Energy

Besides boosting innovation, decarbonisation represents an important step for sustaining future growth, particularly given the high carbon intensity of Emerging Europe’s current energy mix and the progression of environmental policies. This would increase the energy security from the cost and supply availability perspective. The National Energy and Climate Plans (NECPs) outline a commitment to significant decarbonization of electricity generation across the region centred on renewables and nuclear energy. For example, Romania and Hungary aim to fully eliminate coal from their electricity mix by 2030, while other countries plan substantial reductions in coal dependency. Poland has so far presented the lengthiest transition period with coal scheduled for phase-out only by 2049.

EU Funding: A Lifeline for Convergence

Funding the green transition, digitalisation and innovation relies heavily on the EU funding. Emerging Europe countries have been and remain the main beneficiaries of the EU’s cohesion policy. For 2021-27 budgetary period the EU cohesion policy has set 5 policy objectives to support economic growth that are financed primarily from 4 funds: European Regional Development Fund (ERDF), European Social Fund+ (ESF+), Cohesion Fund (CF) and Just Transition Fund (JTF). Total cohesion policy budget for 2021-27 amounts to €529bn of which 70% is financed from the EU budget and 30% from national budgets. The share of Emerging Europe (Bulgaria, Croatia, Czechia, Estonia, Greece, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia, Slovenia) of the amount to be funded from EU budget amounts to €219bn or 60% of the total (55% in 2014-20 period). The share of allocated funds from 2021-27 cohesion budget to GDP in Emerging Europe stood at 13.5% on average compared to only 1.3% in the rest of the EU.

Besides the grants from the regular multiannual budget, Emerging Europe is enjoying additional support from the post-Covid Recovery and Resilience Facility (RRF) that predominantly focuses on green and digital transitions. The Facility entered into force on 19 February 2021. It finances reforms and investments in EU Member States made from the start of the pandemic in February 2020 until 31 December 2026. Of the total RRF grants and loans (€673bn) Emerging Europe has been allocated 27% or €175.5bn. This equates to 11% of 2019 GDP and is split 55% to 45% between grants and loans. The RRF facility in the rest of the EU amounts to only 4% of the 2019 GDP.

Convergence is Real, But Not Guaranteed

We believe that while Emerging Europe countries have the potential to fully converge to Western Europe, this will necessitate a shift in the growth model from one driven by exports (reliant on FDI inflows and low-cost labour) to a model centred on productivity, supported by financial deepening and innovation. There is strong continuing financial support from the EU that in combination with financial market deepening and entrepreneur-friendly policy setting create a solid foundation for continuing productivity growth. It is worth noting that this transition is not that urgent in less developed countries (e.g. Bulgaria, Romania, Turkey), where export-led strategy may continue to yield positive results in the near term.